On March 27th of this year, Congress passed the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), Pub. L. 116-136, which directly addressed the COVID-19 pandemic and relief to millions affected. While the CARES Act addressed a broad array of relief to Americans, one part of the Act amended the FCRA to provide additional requirements upon credit reporting agencies and furnishers in light of the pandemic.

It is undeniable that the impact of the COVID-19 virus has been far-reaching. In a coherent effort to curtail the spread of COVID-19, states issued orders limiting the operations of many businesses and their employees, significantly impacting the financial well-being of each alike. Consequently, many Americans have been faced with the predicament of having to continue to pay their existing obligations without the income or ability to pay. Many find themselves in this situation for the first time – victims of a virus and a response that caused unforeseeable and unthinkable economic turmoil. Thus, consumers have turned to their creditors to seek short-term help to avoid or cure default. Similarly, creditors have welcomed these workouts to bridge the gap from now to the “new normal” that we all equally and eagerly await.

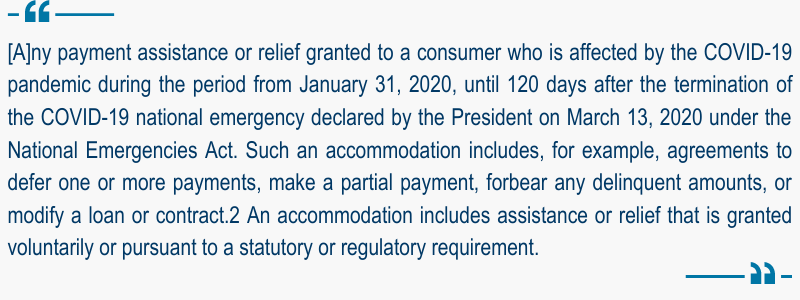

The CARES Act sought to address this situation and ensure that a wave of credit default reporting would be measured given these unprecedented circumstances, providing new requirements for reporting loan workouts. Accordingly, Section 4021 of the CARES Act provides that a consumer whose obligation was not previously delinquent before the pandemic is considered current on their loan or account if they have received an accommodation and they are current in any payments pursuant to the terms of the accommodation. The CFPB states an accommodation includes:

For example, if a consumer was otherwise current on an obligation, but their income was cut due to reduced hours, job loss, etc., and they could foresee default on the horizon, they may sensibly contact the creditor to discuss options such as a modification, forbearance, loan workout or similar “accommodation.” If the parties reach an agreement, the new amendment provides that the creditor cannot report that loan as being in default so long as the consumer adheres to the terms of the accommodation. The FCRA and the CARES Act do not require that a creditor provide an accommodation to a borrower affected by COVID-19, unless the loan at issue is either a federally-backed mortgage loan or a federally-held student loan, both of which are defined in the CARES Act.

Additionally, if an obligation was already delinquent when the accommodation was sought, the CARES Act provides the furnisher cannot advance the delinquent status. Thus, if at the time of the accommodation the consumer was 30 days past due, once the accommodation is made and the terms are being met, the furnisher cannot report the account as 60 days past due the next monthly pay period. Moreover, if during the course of the accommodation the indebtedness is cured and the obligation brought current, the furnisher must report the obligation current at that time.

Furthermore, using a special comment code to report the account in forbearance or as a result of a natural or declared disaster does not comply with the CARES Act. As explained above, the CARES Act requires:

The CARES Act sought to address this situation and ensure that a wave of credit default reporting would be measured given these unprecedented circumstances, providing new requirements for reporting loan workouts. Accordingly, Section 4021 of the CARES Act provides that a consumer whose obligation was not previously delinquent before the pandemic is considered current on their loan or account if they have received an accommodation and they are current in any payments pursuant to the terms of the accommodation. The CFPB states an accommodation includes:

For example, if a consumer was otherwise current on an obligation, but their income was cut due to reduced hours, job loss, etc., and they could foresee default on the horizon, they may sensibly contact the creditor to discuss options such as a modification, forbearance, loan workout or similar “accommodation.” If the parties reach an agreement, the new amendment provides that the creditor cannot report that loan as being in default so long as the consumer adheres to the terms of the accommodation. The FCRA and the CARES Act do not require that a creditor provide an accommodation to a borrower affected by COVID-19, unless the loan at issue is either a federally-backed mortgage loan or a federally-held student loan, both of which are defined in the CARES Act.

Additionally, if an obligation was already delinquent when the accommodation was sought, the CARES Act provides the furnisher cannot advance the delinquent status. Thus, if at the time of the accommodation the consumer was 30 days past due, once the accommodation is made and the terms are being met, the furnisher cannot report the account as 60 days past due the next monthly pay period. Moreover, if during the course of the accommodation the indebtedness is cured and the obligation brought current, the furnisher must report the obligation current at that time.

Furthermore, using a special comment code to report the account in forbearance or as a result of a natural or declared disaster does not comply with the CARES Act. As explained above, the CARES Act requires:

- That if the obligation was current prior to the accommodation, it must be reported as current or

- If it was not current, the reporting cannot advance the level of delinquency. The CFPB’s guidance states that furnishing a special comment code indicating impact by a disaster or that a loan is in forbearance does not meet the CARES Act guidelines.

Simply put, the obligation is to be reported current or delinquently not advanced, but no further special comment or status may be used. Be advised that there is one important caveat to these new rules: these CARES Act amendments relating to accommodations do not apply to obligations that have been charged-off.

Another aspect of the FCRA concerns the handling of disputes related to credit reporting. The FCRA mandates that upon receipt of a dispute, furnishers have thirty (30) days to investigate the dispute and respond to the credit reporting agency from which the dispute was received. Given the relief the CARES Act provides to consumers, one would question whether these hard deadlines are flexible or in any way suspended due to COVID-19 given similar hardships confronting furnishers. In recent guidance, the CFPB advised it would “consider the individual circumstances that consumer reporting agencies and furnishers face as a result of the COVID-19 pandemic, but that the expectation is that “good faith efforts to investigate disputes” are made “as quickly as possible.”

Agencies and furnishers alike would be wise to view the CFPB’s flexibility with some skepticism. While the CFPB states they will take into account individual circumstances of each agency or furnisher, any examination of how COVID-19 has impacted their ability to timely conduct and respond to investigations is subjective. Even if an agency or furnisher views its delays as reasonable under the present circumstances, there is no concrete benchmarks provided by the CFPB to advise whether the CFPB will agree with that assessment. In fact, if the CFPB ultimately determines that those circumstances do not support any delay beyond the 30-day timeframe, or that a “good faith effort” was not made under the circumstances, enforcement action may be taken.

Finally, it’s important to note these amendments are temporary, but they may be with us for the foreseeable future. These amended rules apply only during the “covered period,” which is either July 27, 2020, or 120 days after the President declares an end to the national emergency issued March 13, 2020, whichever occurs later. Given that the first period has passed, furnishers and agencies need be aware that these rules remain in place until four months after the COVID-19 national emergency has officially been terminated.

This blog is not a solicitation for business and it is not intended to constitute legal advice on specific matters, create an attorney-client relationship or be legally binding in any way.

This blog is not a solicitation for business and it is not intended to constitute legal advice on specific matters, create an attorney-client relationship or be legally binding in any way.